Employee Benefits Market Check Survey: Employer Actions on OBBBA

The One Big Beautiful Bill Act (OBBBA), enacted in July 2025, impacts a wide variety of workplace issues, and employers are facing important decisions about how these changes may affect their benefit strategies. From the treatment of HSAs and telehealth, to the potential impact of so-called “Trump Accounts,” to adjustments in DCAP limits, student loan repayment, and other provisions, organizations must determine how (and when) to respond.

To better understand employer perspectives, we conducted several polls on August 21 to understand how they are approaching these changes and what actions they may take in the months ahead. The following results highlight where employers stand today.

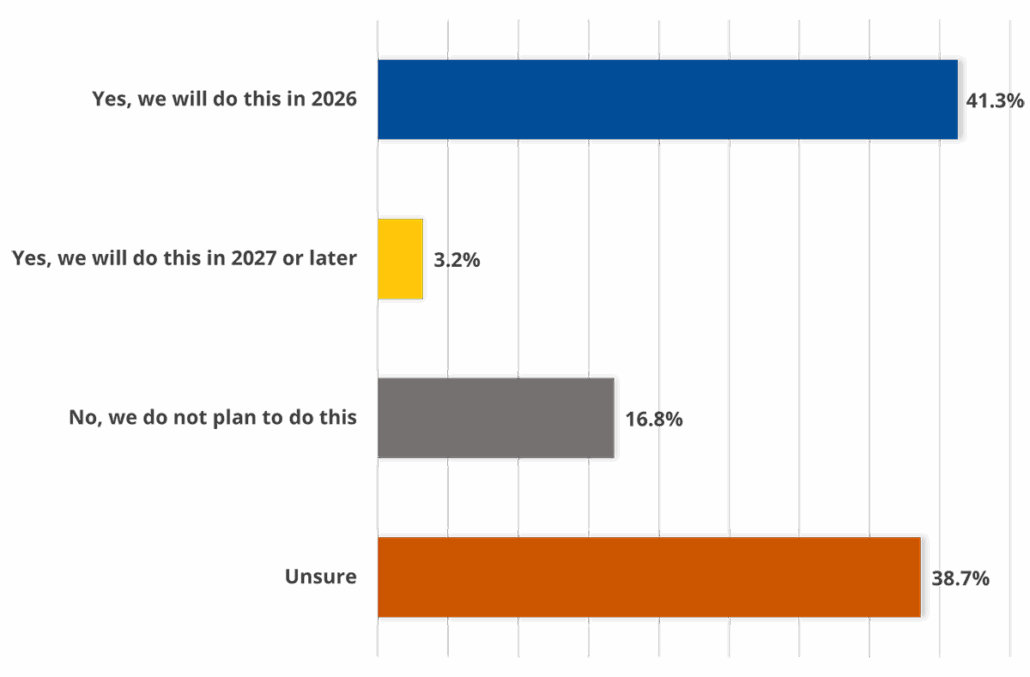

The annual reimbursement limit for a DCAP will increase to $7,500. Will your company increase its limit?

*Results based on 339 employer respondents.

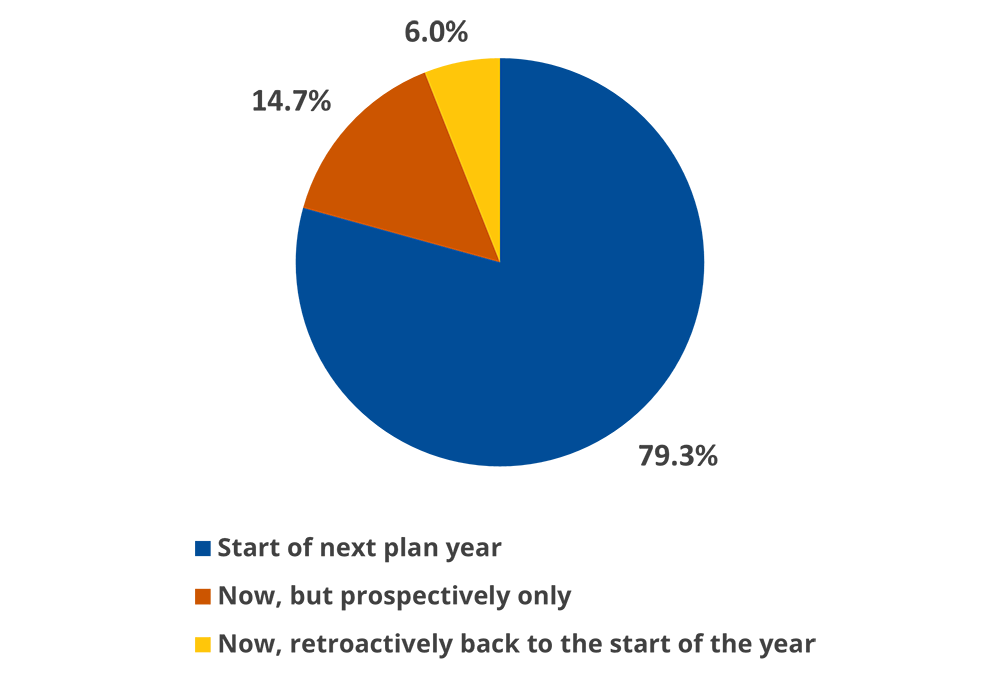

HSAs: When do you intend to eliminate the Fair Market Value fee for use of telehealth?

Other Highlights

The OBBBA permanently allows employers to make tax free student loan reimbursement payments of $5,250 per year, beginning in 2026. Only 2.5% of employers said they will now begin making student loan payments (another 10% indicated they already offer repayment assistance)

The OBBBA creates “Trump Accounts” to promote long-term saving for children. Employers may contribute $2,500 per year per dependent child. Only 2% of employers are committed to contributing in 2026 or later. Another 51% say they are Unsure.

Key Findings

With the OBBBA only having passed recently, there is much to digest. There are some positive changes included in the bill that affect employee benefit plans. Many are still unsure whether they will adopt any of the changes included in the bill, and that is understandable. As annual enrollment draws near for many businesses, leaders should incorporate OBBBA benefit planning into their overall strategy for 2026 and beyond, with the DCAP limit decision being a critical one. While the message of increasing the limit will be positive, employers must be careful to avoid failing the non-discrimination test.

The workforce’s demands will continue to evolve, and plan sponsors should continue evaluating their offerings to ensure they meet the employees’ needs. Clear communication is always critical and will be even more so for the upcoming year.

Should you have any questions regarding any of this information or want to discuss the OBBBA in greater detail, please contact your local Assurex Global adviser.

Leave a Reply

Want to join the discussion?Feel free to contribute!